For investors and lenders, the quality of a borrower’s climate disclosure is the primary window into their transition readiness. However, the proliferation of global frameworks has created an “alphabet soup” that often leads to ESG fatigue and asymmetric information risks. Understanding the technical nuances between these frameworks is critical for evaluating whether a borrower is genuinely mitigating risk or merely engaging in tick-box compliance.

Impact versus Financial Materiality in Global Standards

The reporting landscape is fundamentally divided by the concept of materiality.

Dual Materiality (GRI)

The Global Reporting Initiative (GRI) employs the principle of dual materiality. This approach reveals how a company impacts the environment and society (inside-out) and how environmental shifts impact the company (outside-in). It serves as the gold standard for multi-stakeholder transparency while remaining interoperable with financial standards.

Financial Materiality (TCFD & ISSB)

The Task Force on Climate-related Financial Disclosures (TCFD) and the International Sustainability Standards Board (ISSB) focus on financial materiality. These frameworks disclose information that is useful to investors in making resource allocation decisions. IFRS S2 fully incorporates the TCFD’s four-pillar architecture, which includes Governance, Strategy, Risk Management, and Metrics/Targets, creating a global baseline that connects climate performance directly to enterprise value.

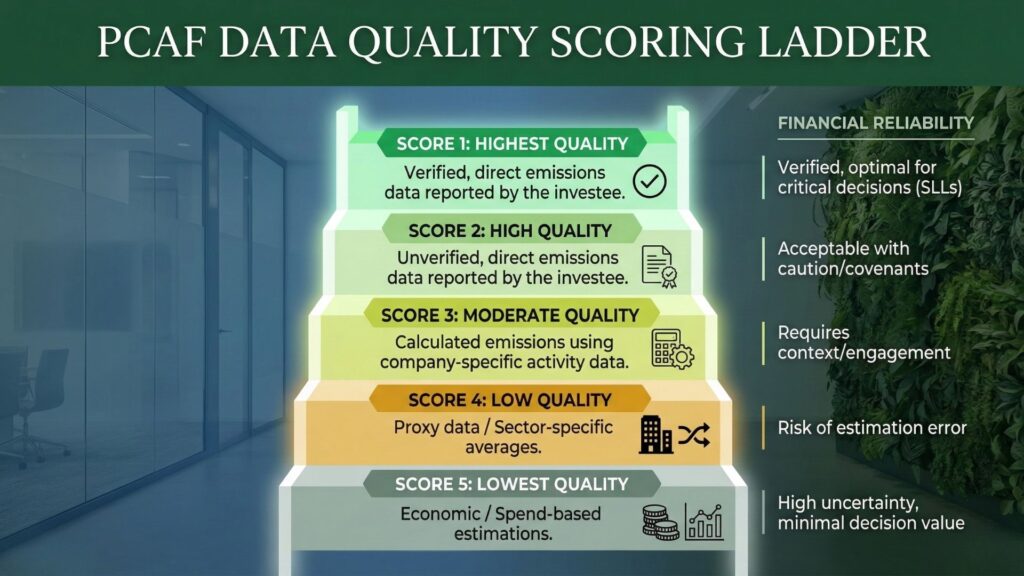

The PCAF Data Quality Scoring System

The Partnership for Carbon Accounting Financials (PCAF) is specifically designed for the financial industry to quantify financed emissions (Scope 3, Category 15). The heart of the PCAF methodology is a five-tier scoring system that communicates the confidence level of emissions data. Score 1 represents the highest quality, involving verified direct emissions data reported by the investee. Score 5, the lowest, relies on economic estimations based on broad spend data or sector averages. The 2025 PCAF updates have expanded this scope to include methodologies for “Use of Proceeds” structures and “sub-sovereign debt,” allowing banks to report on regional and municipal government bonds with greater precision.

| PCAF Score | Data Quality | Source Description | Reliability for Finance |

| 1 | Highest | Verified, direct emissions from investee | Primary choice for SLLs |

| 2 | High | Unverified, direct emissions from investee | Acceptable with covenants |

| 3 | Moderate | Calculated from company-specific activity data | Requires engagement |

| 4 | Low | Proxy data / Sector-specific averages | Risk of under-provisioning |

| 5 | Lowest | Economic / Spend-based estimations | High uncertainty |

Investors and lenders should look for “connected information”—the explicit linkage between a borrower’s disclosed climate risks and their financial statement line items. Disclosures that lack board oversight details (currently only disclosed by 25% of firms) or fail to use forward-looking climate scenario analysis should be flagged as high-risk during the due diligence process.

The 2025 PCAF updates have expanded this standard to cover 10 asset classes, including Use of Proceeds structures and sub-sovereign debt, allowing banks to report on regional and municipal government bonds with greater precision.

Strategic Pro Tips for Evaluating Disclosure Quality

To move beyond optics and ensure disclosures deliver genuine value, lenders should look for:

- Audit the Connected Information: Seek the explicit linkage between a borrower’s disclosed climate risks and their financial statement line items. Disclosures that treat ESG as a separate narrative without financial quantification are a high-risk indicator.

- Mandate Climate Scenario Analysis: IFRS S2 specifically requires companies to explain the resilience of their strategy using climate-related scenario analysis. Lenders should flag any disclosure that lacks this forward-looking modeling as insufficient for credit risk pricing.

- Verify Governance Process, Not Just State: Avoid tick-box governance reporting. High-quality disclosures detail the exact frequency and process by which the board is informed of climate risks, rather than just stating oversight exists.

- Scrutinize Transition Plan Resource Allocation: A transition plan is more than a goal; it must include critical assumptions and how the company is resourcing the activities outlined. Plans without clear CapEx commitments are likely window dressing.

Conclusion

Standardized climate disclosure is the foundation of efficient capital allocation. By comparing frameworks and applying rigorous data quality scores, financial institutions can identify high-integrity borrowers and mitigate the risks of greenwashing.

Ready to bridge the gap between disclosure and capital allocation? Contact for expert advice to refine your transition risk due diligence or to integrate PCAF data quality scoring into your lending framework. Click here to get in touch.

This article was written by Virna Chávez from the Green Initiative Team.

FAQ – Frequently Asked Questions

The primary difference lies in materiality. TCFD (Task Force on Climate-related Financial Disclosures) focuses on financial materiality—how climate change affects the company’s bottom line. GRI (Global Reporting Initiative) uses “dual materiality,” which tracks both the company’s financial risks and its external impact on the environment and society.

The PCAF (Partnership for Carbon Accounting Financials) score is a 1-to-5 ranking used to communicate the reliability of carbon emissions data. A Score 1 represents the highest quality (verified direct data), while a Score 5 represents the lowest quality (estimated data based on economic spend).

IFRS S2, issued by the International Sustainability Standards Board (ISSB), fully incorporates the TCFD’s four-pillar architecture (Governance, Strategy, Risk Management, and Metrics/Targets). It is designed to be the global baseline for climate-related financial disclosures.

Climate scenario analysis is a forward-looking tool that tests a borrower’s resilience against various future climate paths (e.g., a 1.5°C vs. 3°C world). For lenders, it is critical for accurate credit risk pricing and identifying long-term transition readiness.

Financed emissions (Scope 3, Category 15) are the greenhouse gas emissions associated with a financial institution’s loans, investments, and insurance underwriting. Tracking these is essential for banks to align their portfolios with Net Zero targets.

References & Further Reading

- BDO. (2025). Common pitfalls in climate reporting. https://www.bdo.co.uk/en-gb/insights/audit-and-assurance/common-pitfalls-in-climate-reporting

- IFRS Foundation. (2024, November). Comparison: IFRS S2 climate-related disclosures with the TCFD recommendations. https://www.ifrs.org/content/dam/ifrs/supporting-implementation/ifrs-s2/ifrs-s2-comparison-tcfd.pdf

- Partnership for Carbon Accounting Financials. (2025, December 2). Financed emissions standard part A. (https://carbonaccountingfinancials.com/files/standard-launch-2025/PCAF-PartA-2025-Full-Document-Clean.pdf)