Financial markets are currently undergoing a fundamental transition from “proceeds-based” financing to “performance-linked” structures. In the early stages of green finance, capital was simply earmarked for specific assets like wind farms or solar arrays. Today, Sustainability-Linked Loans (SLLs) and Bonds (SLBs) have effectively transformed climate performance into a financial covenant.

Defining Performance-Linked Finance

Sustainability-Linked Loans are corporate financing tools where the cost of capital, most commonly the interest rate, is directly linked to the borrower’s achievement of predefined Sustainability Performance Targets (SPTs). These instruments allow proceeds to be used for general corporate purposes, which distinguishes them from traditional green loans that require funds to be earmarked for specific environmental projects.

Similarly, Sustainability-Linked Bonds are debt instruments where the issuer commits to reaching specific sustainability milestones. The financial or structural characteristics of the bond, such as the coupon rate, adjust based on the achievement of these targets. By utilizing margin ratchets, which are interest rate adjustments typically ranging from 5 to 25 basis points, lenders can incentivize corporate behavior directly.

However, this evolution creates a technical paradox: for these incentives to be credible, they must be supported by high-fidelity data. If the cost of Monitoring, Reporting, and Verification (MRV) exceeds the financial benefit of the greenium, which is the interest rate discount, the instrument becomes economically unviable for the borrower and a reputational risk for the lender. To solve this, financial institutions must align their MRV investment with the scale and complexity of their portfolios.

Why MRV Infrastructure Matters in Modern Finance

The global transition to a net-zero economy has triggered a structural shift in climate finance. Performance-based climate finance requires robust monitoring systems to turn climate resilience into a priced managerial obligation. Institutions must move from subjective reporting to objective evidence to maintain market integrity.

The current landscape shows that median baseline uncertainty in manual systems can span 171% of the mean estimate. This variability leads to over-crediting or inaccurate margin adjustments. High-integrity infrastructure uses multi-model ensemble approaches and historical geospatial data to reduce this variability.

Navigating the MRV Evolution: A Sophistication Roadmap

Institutional investment in MRV is generally categorized into three tiers based on asset size and the scale of sustainability-linked operations. Building a high-integrity “truth layer” requires a phased approach that balances capital expenditure (CapEx) against long-term operational savings.

Tier 1: Small Institutions (<€1bn assets)

Small institutions, typically those with less than €1 billion in sustainability-linked assets, often rely on Tier 1 methodologies. These prioritize minimizing upfront capital expenditure (CapEx) by using IPCC default factors—generic emission values provided for different activities—and manual reporting templates. The primary objective for these players is to reduce the administrative burden while maintaining a basic level of compliance that satisfies regulatory “tick-box” requirements. While accessible, this approach suffers from a significant “audit lag,” where verification cycles take 12 to 24 months, potentially creating “asymmetric information” risks where lenders cannot verify if a performance target was truly met.

Tier 2: Mid-Sized Institutions (€1bn–€30bn assets)

Mid-sized institutions represent the segment transitioning toward digitalized data ingestion. By utilizing cloud-based databases to aggregate borrower data, these institutions reduce manual reconciliation labor costs, which can otherwise reach $250,000 annually for a moderate portfolio. This phase focuses on efficiency and the standardization of reporting across different sectors to facilitate portfolio-wide risk assessment. By integrating third-party data, such as satellite-derived land-use changes, FIs can establish a more consistent and objective baseline for performance tracking.

Tier 3: Large Institutions (>€30bn assets)

Large institutions benefit from significant economies of scale by investing in full Digital MRV (dMRV). Although the initial CapEx is higher, the operational expenditure (OpEx) of verification is reduced by an estimated 50–70% through automation and the removal of physical site-visit requirements. For these entities, dMRV is not just a compliance tool but a strategic differentiator that allows them to offer more competitive terms and attract ESG-focused capital at lower costs. This transition enables “Internet Audits” where hardware and software are certified once, allowing for subsequent verifications to be conducted remotely.

| Institutional Tier | Asset Threshold | MRV Methodology | Financial Result |

| Small | <€1bn | Tier 1 (IPCC Defaults) | Low CapEx / High labor |

| Mid-Sized | €1bn–€30bn | Digitalized Cloud | Reconciliation Savings |

| Large | >€30bn | Full dMRV / IoT | 50–70% OpEx reduction |

Step-by-Step Implementation of MRV Infrastructure

To build a high-integrity truth layer, financial institutions should follow this phased roadmap :

Step 1: Map the Current Data Landscape

Evaluate existing portfolio management systems and identify where emissions data is missing or estimated. This assessment allows lenders to prioritize sectors with high materiality, such as energy utilities or heavy manufacturing.

Step 2: Establish Sophistication Tiers

Align investment with portfolio size. Small institutions (<€1bn assets) often rely on Tier 1 methodologies using IPCC default factors. Mid-sized institutions (€1bn–€30bn assets) transition toward digitalized ingestion using cloud databases to reduce manual reconciliation costs. Large institutions (>€30bn assets) invest in full Digital MRV (dMRV) to benefit from economies of scale.

Step 3: Identify “DMRV Hotspots”

The efficiency frontier targets the highest possible integrity-to-cost ratio rather than achieving 100% accuracy everywhere. Lenders should digitize priority workflow components, such as automated emission reduction (ER) calculations and third-party verification, where manual processes are slow and resource-intensive.

Step 4: Deploy Middleware Gateways

FIs should deploy a middleware layer to facilitate secure, real-time data ingestion from dMRV platforms rather than replacing legacy core banking systems. API gateways act as translators between IoT sensor data and traditional banking formats.

Step 5: Align with Accredited Verifiers

The ultimate guarantor of trust is the third-party verifier. For performance-based finance, verifiers must be accredited under international standards such as ISO 14064-3 and ISO 14065.

Strategic Pro Tips for Implementation

To transition from a “tick-box” compliance exercise to a high-value strategic operation, financial institutions should consider these advanced integration strategies:

1. Hard-wire Internal Carbon Pricing (ICP)

Global best practice is moving beyond “token fees” or “shadow prices” used only for theoretical reporting. Effective ICP must be hard-wired into capital expenditure (CapEx) approvals, ensuring no project receives approval unless it remains viable under the internal carbon price. This strategy is essential for firms preparing for compliance landscapes like the Indian Carbon Market (ICM) and its Carbon Credit Trading Scheme (CCTS), which puts a financial price on actual greenhouse gas emissions. Institutions should benchmark their ICP against external signals; for example, setting a tiered price starting at ₹1,500/t in 2025 and scaling to ₹3,000/t by 2030 helps signal the real cost of transition to borrowers and incentivize more aggressive decarbonization before domestic schemes tighten.

2. Focus on “DMRV Hotspots” for Maximum ROI

The “Efficiency Frontier” is not about achieving 100% accuracy across every data point; it is about finding the highest possible integrity-to-cost ratio rather than achieving 100% accuracy everywhere. Lenders should identify priority workflow components, or DMRV hotspots, where digitization delivers the greatest value, such as automated emission reduction (ER) calculations and third-party verification. High-priority areas typically include manual processes that are historically slow, error-prone, and resource-intensive. By weighing the benefits of advanced sensing against less complex but readily available alternatives, banks can scale their portfolios more cost-effectively.

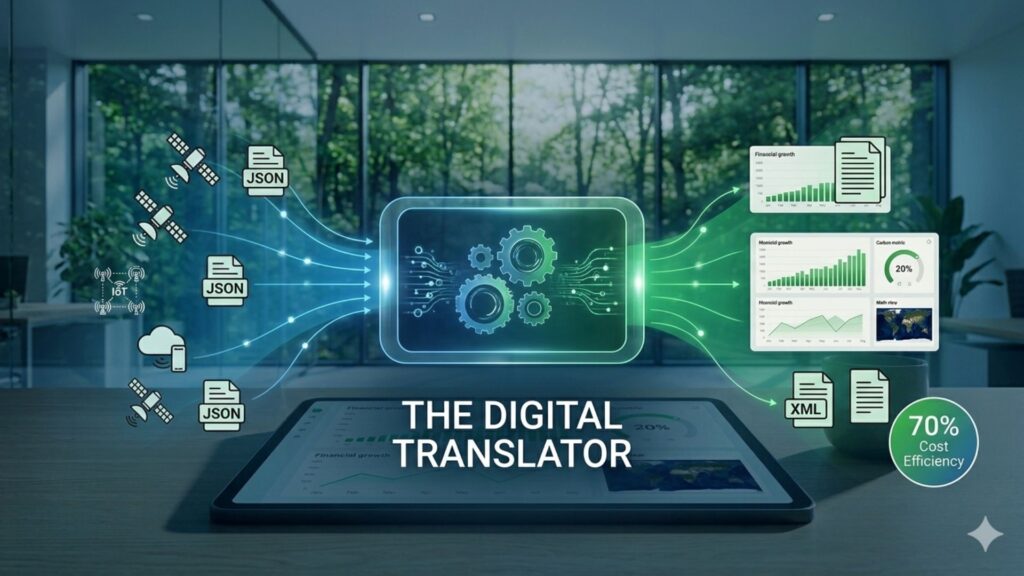

3. Deploy API Gateways as “Digital Translators”

Rather than attempting a multi-year overhaul of legacy core banking systems, FIs should deploy a middleware layer. API gateways act as “translators” between the diverse technical “dialects” of the climate economy—for example, converting JSON data from IoT sensors into the XML formats required by traditional banking platforms.

Leading gateways, such as Tyk, can offer up to 70% cost savings through cloud-native architecture while providing the centralized control needed to onboard fintech partners instantly and automate compliance.

Utilizing a platform with built-in integrations can eliminate data silos, giving the board a unified “source of truth” across procurement, project management, and risk departments.

4. Adopt Digital Systems from “Day One”

One of the most common pitfalls is delaying MRV implementation, which often leads to “data gaps” that are impossible or prohibitively expensive to fix later. Retrofitting historical production data is notoriously messy and can derail certification, potentially sinking a bid even if the underlying project is viable. By establishing a digital backbone from the start, institutions ensure that every ton of carbon is quantifiable, traceable, and verifiable, protecting long-term revenue potential and enhancing buyer confidence.

Frequently Asked Questions (FAQ)

A basis point is a standard unit of measurement in finance representing one-hundredth of one percent (0.01%). In sustainability-linked instruments, basis points are used to express tiny variations in interest rates with absolute precision. This eliminates confusion between relative and absolute percentage changes. For example, an adjustment of 25 basis points corresponds to a shift of exactly 0.25%.

The 5 to 25 bps bracket is the established market convention for performance-linked incentives in Sustainability-Linked Loans. This range is currently more conservative than traditional financial facility ratchets, which customarily reduce interest across a range of 10 to 50 basis points. Lenders often maintain these increments because performance-linked terms are a relatively new innovation. This cautious approach allows market participants to test target scrutiny in practice before wider, more material financial impacts are adopted.

The “greenium” refers to the interest rate discount a borrower receives for meeting sustainability targets. It acts as a financial incentive to improve environmental performance. However, the borrower must ensure that the cost of Monitoring, Reporting, and Verification (MRV) does not exceed this discount, or the instrument becomes economically unviable.

DMRV Hotspots are specific workflow components—such as automated emission reduction (ER) calculations or third-party verification—where digitization offers the highest integrity-to-cost ratio. Rather than trying to achieve 100% accuracy across every single data point, focusing on these hotspots allows financial institutions to scale their portfolios cost-effectively while eliminating slow, error-prone manual processes.

Attempting a full overhaul of legacy core banking systems is often a multi-year, prohibitively expensive project. An API gateway acts as a “digital translator” (middleware), converting modern data formats from IoT sensors into the traditional formats required by existing banking platforms. This approach can offer up to 70% cost savings and allows institutions to onboard new fintech partners and automate compliance almost instantly.

This article was written by Virna Chávez from the Green Initiative Team.

References & Further Reading

Anaxee. (2025, July 28). Winning beyond compliance: How carbon markets can sharpen your competitive edge. https://anaxee.com/winning-beyond-compliance-how-carbon-markets-can-sharpen-your-competitive-edge/

Carbonfuture. (2025, October 8). 7 reasons leading carbon removal suppliers use digital MRV from day one. https://www.carbonfuture.earth/magazine/7-reasons-leading-carbon-removal-suppliers-use-digital-mrv-from-day-one

Lawrbit. (2026, January). Comprehensive legal framework for the Carbon Credit Trading Scheme (CCTS). https://www.lawrbit.com/article/carbon-credit-trading-scheme/

Partnership for Carbon Accounting Financials. (2025, December 2). The global GHG accounting and reporting standard for the financial industry.(https://carbonaccountingfinancials.com/files/standard-launch-2025/PCAF-PartA-2025-Full-Document-Clean.pdf)

Tyk Technologies. (2025). API management for financial services: Modernizing for open finance. https://tyk.io/financial-services/

World Bank Carbon Markets Infrastructure Working Group. (2025, June). Technical guidance note on standardizing digital MRV in carbon markets: System evaluation criteria and hotspots assessment. https://openknowledge.worldbank.org/entities/publication/397c4e52-445a-4cf4-89df-f2e61373a524